The question is Roth pre or post tax trips up more people than you’d think—and for good reason. The answer directly impacts how much money stays in your pocket and how much you owe Uncle Sam later. Here’s the straightforward truth: Roth contributions are made with after-tax dollars, meaning you’ve already paid income tax on the money before it goes into your account. This is fundamentally different from traditional pre-tax retirement accounts, and understanding this distinction could save you thousands over your lifetime.

Table of Contents

Roth Basics: After-Tax Reality

Let’s cut through the confusion right away. When you contribute to a Roth account—whether it’s a Roth IRA or Roth 401(k)—you’re using money that’s already been taxed. If you earn $50,000 and contribute $7,000 to a Roth IRA, that $7,000 came from your take-home pay after federal, state, and local taxes were already withheld.

This is the opposite of traditional retirement accounts. With a traditional IRA or traditional 401(k), your contributions reduce your taxable income in the year you make them. You get an immediate tax break, but you’ll owe taxes later when you withdraw the money in retirement.

The Roth approach flips this script. You pay taxes now, contribute after-tax money, and then—here’s the magic—all future growth and withdrawals are completely tax-free. No taxes on earnings, no taxes on distributions. This is why financial advisors often call Roth accounts “tax-free growth machines.”

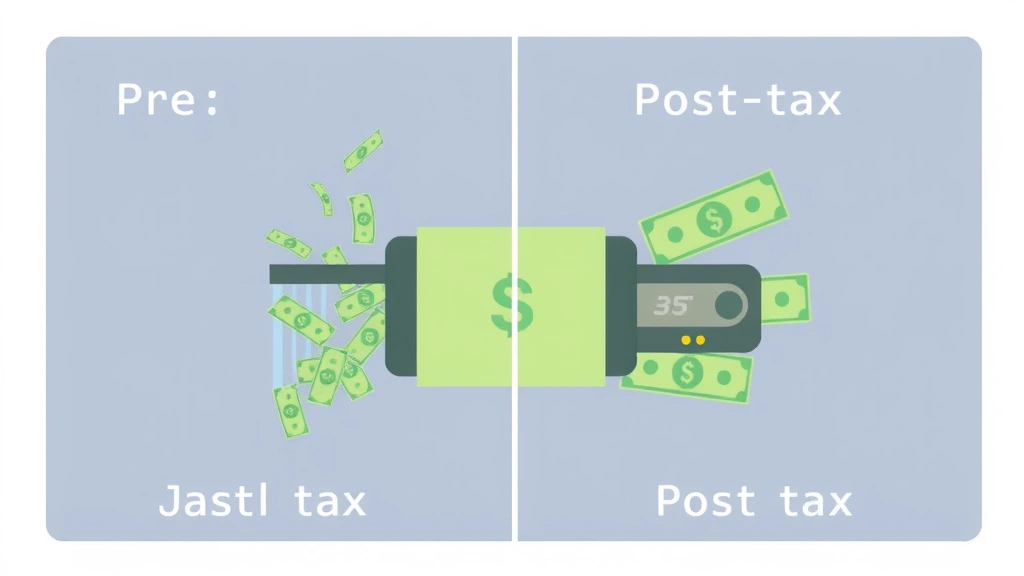

Pre-Tax vs. Post-Tax Explained

Understanding the difference between pre-tax and post-tax contributions is essential for optimizing your retirement strategy. Think of your paycheck as a pie. Pre-tax contributions slice off a piece before taxes are calculated. Post-tax contributions come from what’s left after the IRS takes its cut.

Pre-tax contributions:

- Reduce your current taxable income

- Lower your federal income tax bill this year

- Grow tax-deferred (you don’t pay taxes on earnings until withdrawal)

- Subject to income taxes when you withdraw in retirement

- Helpful if you’re in a high tax bracket now

Post-tax contributions:

- Don’t reduce your current taxable income

- No immediate tax benefit

- Grow completely tax-free

- Withdrawals are 100% tax-free in retirement

- Ideal if you expect to be in a higher tax bracket later

This distinction matters enormously. If you’re young and expect your income to rise significantly, Roth’s post-tax structure often wins. If you’re in peak earning years and need to reduce taxable income now, traditional pre-tax accounts might make more sense. Many people benefit from a mix of both.

How Roth IRA Works

A Roth IRA is an individual retirement account where post-tax contributions grow tax-free. For 2024, you can contribute up to $7,000 per year (or $8,000 if you’re 50 or older). The money you contribute has already had income tax withheld from your paycheck.

Here’s what happens inside your Roth IRA:

- You deposit after-tax money

- You invest it in stocks, bonds, mutual funds, or other securities

- Those investments grow over decades

- You never pay taxes on that growth

- You can withdraw contributions anytime, tax-free

- After age 59½, you can withdraw earnings tax-free if the account is 5+ years old

The beauty of Roth IRAs is flexibility. Unlike traditional IRAs, there’s no required minimum distribution (RMD) at age 73. You can let that money compound forever if you want. You can also withdraw your contributions (not earnings) anytime without penalty, making it a pseudo-emergency fund.

However, there are income limits. For 2024, if you’re single and earn more than $161,000 (or $240,000 if married filing jointly), you can’t contribute directly to a Roth IRA. This is where the “backdoor Roth” strategy comes in—a legal workaround that lets high earners fund Roth accounts indirectly.

Roth 401(k) Mechanics

A Roth 401(k) is your employer’s version of the Roth concept. Some employers offer both traditional and Roth 401(k) options. Like a Roth IRA, contributions are made with post-tax dollars, and growth is tax-free.

Key differences from Roth IRAs:

- Higher contribution limits: $23,500 per year in 2024 ($31,000 if 50+)

- No income limits—everyone can contribute regardless of earnings

- Employer matching is always pre-tax (this is important!)

- Required minimum distributions apply at age 73

- You can borrow against your balance (generally not allowed with IRAs)

- Stricter withdrawal rules before age 59½

Here’s a critical detail: if your employer matches your 401(k) contributions, that match goes into a traditional (pre-tax) account. You can’t have matching contributions in Roth. So if you contribute $500 post-tax to your Roth 401(k) and your employer matches with $500, that match lands in a separate traditional 401(k) bucket. You’ll owe taxes on that match when you withdraw it later.

This dual-bucket reality is why many people use Roth 401(k)s strategically. You get the post-tax advantage on your own contributions, but understand that employer matches maintain their pre-tax status.

Tax Implications You Need

The tax implications of choosing Roth accounts are profound and long-lasting. Let’s walk through a realistic scenario.

Imagine you’re 30 years old, earning $80,000 annually, and can save $10,000 per year. You have two paths:

Path A: Traditional 401(k) (pre-tax)

You contribute $10,000 pre-tax. Your taxable income drops from $80,000 to $70,000. At a 22% federal tax rate, you save $2,200 in taxes immediately. That $10,000 grows tax-deferred for 35 years. If it grows to $150,000, you’ll owe taxes on the full $150,000 when you withdraw it in retirement.

Path B: Roth 401(k) (post-tax)

You contribute $10,000 from after-tax income. You don’t get the immediate $2,200 tax break. But that $10,000 grows to $150,000 completely tax-free. At retirement, you withdraw the full $150,000 with zero tax bill.

The question is: which tax rate is lower—your current 22% or your retirement tax rate? If you expect to be in a lower bracket in retirement (maybe you stop working, your income drops), traditional pre-tax wins. If you expect to be in the same or higher bracket, Roth wins.

Most financial advisors suggest this rule of thumb: if you’re in the 22% bracket or lower now, lean Roth. If you’re in the 32% bracket or higher, lean traditional. It’s not a perfect formula, but it captures the essence of the decision.

Also consider state taxes. Some states don’t tax retirement income, which can make Roth even more attractive if you plan to retire there. Understanding how taxes are deducted at the source helps you plan these scenarios accurately.

Withdrawal Rules Matter

Roth withdrawal rules are unique and need careful attention. The IRS has specific ordering rules for Roth distributions, and violating them can trigger unexpected taxes.

Roth IRA withdrawal order:

- Contributions (always tax and penalty-free)

- Conversions (pro-rata rule applies)

- Earnings (taxable if withdrawn before age 59½ and account isn’t 5+ years old)

This ordering is crucial. If you contributed $50,000 to a Roth IRA over your lifetime and it grew to $150,000, you can withdraw $50,000 anytime without tax or penalty. The first dollars out are always your contributions.

However, if you did a backdoor Roth conversion (converting pre-tax IRA money to Roth), things get complicated. The IRS applies a “pro-rata rule” that considers all your pre-tax and post-tax IRA balances together. If you have $100,000 in a traditional IRA and convert $10,000 to Roth, a portion of that conversion is taxable based on your total IRA balance.

Roth 401(k) withdrawal rules are stricter. You generally can’t withdraw before age 59½ without a 10% penalty (with limited exceptions like disability or hardship). But after 59½, you can withdraw your contributions and earnings tax-free.

Income Limits & Eligibility

Income limits are where many people hit a wall with Roth IRAs. For 2024, direct Roth IRA contributions are limited if you earn:

- Single: Phase-out begins at $146,000, eliminated at $161,000

- Married filing jointly: Phase-out begins at $230,000, eliminated at $240,000

- Married filing separately: Phase-out begins at $0, eliminated at $10,000

If you exceed these limits, you can’t contribute directly to a Roth IRA. But there’s a workaround: the “backdoor Roth.” You contribute to a traditional IRA (no income limits), then immediately convert it to a Roth IRA. This is legal and used by millions of high earners.

Roth 401(k)s have no income limits. Anyone can contribute, regardless of earnings. This makes them attractive for high-income earners who want post-tax retirement savings.

Also check your AGI on your tax return to confirm you’re within limits. AGI (Adjusted Gross Income) is what the IRS uses for these determinations, not gross salary.

Strategy: Which Works Best

Choosing between Roth and traditional accounts isn’t one-size-fits-all. Here’s how to think about it strategically.

Choose Roth if:

- You’re young (time is your biggest asset)

- You’re in a low tax bracket now

- You expect significant income growth

- You expect tax rates to rise in the future

- You want flexibility in withdrawals

- You want to minimize required distributions

- You want to leave tax-free money to heirs

Choose Traditional if:

- You’re in a high tax bracket now

- You need to reduce taxable income this year

- You expect to be in a lower bracket in retirement

- You want the immediate tax deduction

- You have limited cash flow and the tax savings help

Many financial experts suggest a “barbell” approach: max out traditional contributions to get the immediate tax break and reduce current taxable income, then use any remaining savings capacity for Roth. This gives you tax diversification—some money taxed now, some taxed later, letting you optimize withdrawals in retirement.

For specific guidance on your paycheck and withholding strategy, understanding paycheck optimization can help you see how pre-tax contributions affect your take-home pay.

Consider also that medical insurance is pre-tax, which means you’re already using pre-tax strategies for health expenses. Balancing this with Roth retirement savings creates a comprehensive tax strategy.

Frequently Asked Questions

Is a Roth IRA pre-tax or post-tax?

A Roth IRA is funded with post-tax dollars. You contribute money that’s already had income tax withheld. In exchange, all growth and withdrawals are completely tax-free. There’s no immediate tax deduction, but the long-term tax savings can be substantial.

Can I contribute to both Roth and traditional accounts?

Yes, you can contribute to both. However, your total contributions to all IRAs (traditional, Roth, SEP, and SIMPLE combined) can’t exceed the annual limit ($7,000 for 2024). For 401(k)s, you can contribute to both traditional and Roth versions if your employer offers both, but the combined limit is $23,500 in 2024. Employer matching contributions don’t count toward your limit.

When should I do a backdoor Roth?

Do a backdoor Roth if you earn above the income limits for direct Roth IRA contributions and want to fund a Roth account. The process is simple: contribute to a traditional IRA, then immediately convert it to a Roth IRA. Be aware of the pro-rata rule if you have other pre-tax IRA balances. Timing matters—do the conversion in the same tax year as the contribution.

What happens to Roth money if I die?

Roth accounts pass to heirs tax-free. Your beneficiaries inherit the account and can withdraw the money without paying income taxes. This makes Roth accounts excellent for estate planning, especially if you expect significant growth. However, heirs must follow required distribution rules (they generally must empty the account within 10 years under current law).

Can I withdraw from my Roth IRA before retirement?

You can withdraw your contributions anytime, tax and penalty-free. Withdrawing earnings before age 59½ typically triggers a 10% penalty and income taxes, unless you qualify for an exception (like first-time home purchase up to $10,000, disability, or medical expenses). This flexibility makes Roth IRAs useful as a backup emergency fund.

Do Roth 401(k) employer matches get taxed?

Yes. While your Roth 401(k) contributions are post-tax, employer matching contributions are always pre-tax and go into a separate traditional account. You’ll owe taxes on that match when you withdraw it in retirement. This is a key distinction many people miss.

What’s the five-year rule for Roth accounts?

The five-year rule states that you must have owned your Roth IRA for at least five tax years to withdraw earnings tax-free (after age 59½). The clock starts January 1 of the year you open your first Roth IRA. Conversions have their own five-year rule—you must wait five years after a conversion before withdrawing those converted funds penalty-free.

Final Thoughts: Making Your Decision

So, is Roth pre or post tax? It’s post-tax, and that simple fact reshapes your entire retirement savings strategy. Roth contributions use after-tax money, but the payoff is tax-free growth and tax-free withdrawals forever.

The decision between Roth and traditional accounts isn’t about which is objectively “better”—it’s about which matches your personal situation. Your age, current tax bracket, expected retirement income, and time horizon all matter. Many people benefit from contributing to both types, creating a diversified retirement portfolio that’s tax-efficient no matter what happens.

If you’re young and can afford it, Roth deserves serious consideration. Time is the most powerful tool in investing, and tax-free growth over 30+ years is genuinely transformative. If you’re in peak earning years and need to reduce taxes now, traditional accounts might win. The key is being intentional about your choice rather than defaulting to whatever your employer offers.

Review your strategy annually. Tax laws change, your income changes, and your retirement timeline shifts. What makes sense at 30 might need adjustment at 45. Work with a tax professional if you’re high-income or have complex situations. The cost of good tax advice pays for itself many times over.