The national school voucher program tax credit represents one of the most significant—and often misunderstood—tax benefits available to families navigating education costs. Whether you’re considering private school tuition, homeschooling expenses, or education savings accounts, understanding how these credits work can put thousands of dollars back in your pocket. As a CPA who’s helped countless families optimize their education-related tax situations, I can tell you that most people leave money on the table simply because they don’t know what’s available to them.

Table of Contents

What Is a School Voucher Tax Credit?

A school voucher tax credit is a tax incentive designed to help families pay for qualified education expenses outside the traditional public school system. Unlike a deduction (which reduces your taxable income), a credit directly reduces the amount of tax you owe—dollar for dollar. If you owe $5,000 in taxes and claim a $2,000 education credit, you now owe $3,000. That’s the power of credits.

The confusion starts here: there’s no single “national” school voucher program. Instead, we have a patchwork of federal education credits and state-specific voucher programs, each with different rules, income limits, and qualifying expenses. Some states offer robust tax credit scholarships; others offer nothing at all. This is where working with a tax strategist becomes invaluable.

Federal vs. State Programs

Here’s where it gets interesting. The federal government offers education credits like the American Opportunity Tax Credit and Lifetime Learning Credit, which apply nationwide but have specific income thresholds and expense limitations. Meanwhile, states have created their own voucher programs—some funded through tax credits—that operate independently.

Federal credits are claimed on your Form 1040 and are subject to income phase-outs. State voucher programs, on the other hand, often function through tax credit scholarships where donors receive a credit against their state income taxes in exchange for funding education scholarships. Arizona’s Empowerment Scholarship Account and Florida’s Step Up For Students are prime examples. The mechanics differ significantly, and the tax treatment can vary dramatically depending on your state of residence.

This distinction matters enormously for your tax planning. A family in Arizona might access a state education tax credit scholarship while simultaneously claiming a federal education credit—but they need to ensure the expenses don’t overlap and create unintended consequences.

Eligibility Requirements Explained

Eligibility for the national school voucher program tax credit depends heavily on which program you’re using. Federal credits have income limits that phase out starting around $80,000-$90,000 for single filers (these adjust annually). State programs vary wildly—some have no income limits, while others restrict participation to families below certain thresholds.

Generally, to qualify for federal education credits, you need:

- A valid Social Security Number for the student

- Enrollment at an eligible educational institution (accredited college, university, or vocational school)

- Qualified education expenses paid in the same tax year

- Income below the phase-out threshold

For state voucher programs, eligibility often depends on factors like prior public school enrollment, income level, or special circumstances (disability, low income, military family status). Some states require that students previously attended public school; others don’t. This is critical—you cannot assume your situation qualifies across state lines.

How Tax Credits Actually Work

Let me break down the mechanics because this is where the real value lives. A tax credit is fundamentally different from a deduction, and understanding this difference can mean the difference between a $2,500 benefit and a $5,000 benefit.

The American Opportunity Tax Credit (AOTC), the most valuable federal education credit, is worth up to $2,500 per student per year. Here’s the structure: $2,000 is non-refundable (meaning it can’t reduce your tax liability below zero), but $500 is refundable (meaning you can get it as a refund even if you owe no taxes). This makes the AOTC particularly valuable for lower-income families.

The Lifetime Learning Credit, by contrast, is worth up to $2,000 per tax return (not per student) and is entirely non-refundable. You can claim either AOTC or Lifetime Learning in the same year, but not both for the same student.

State tax credit scholarships operate differently. Instead of claiming a credit on your personal return, you donate money to a scholarship-granting organization and receive a credit against your state income tax liability. The student then receives a scholarship from that organization. This structure has implications for your federal tax situation—the donation may not be deductible, but the credit reduces your state taxes.

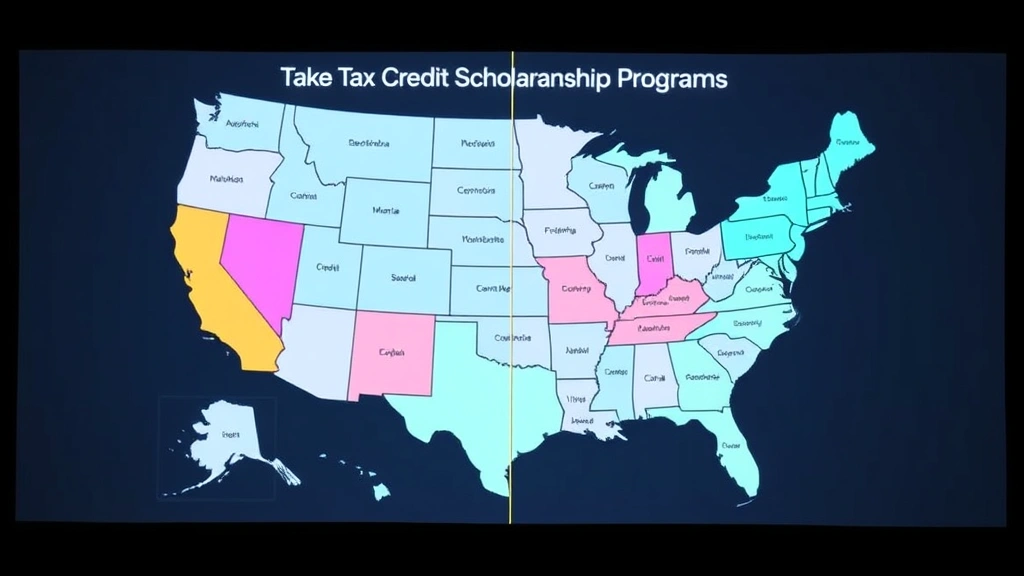

State Voucher Programs Overview

As of 2024, over 20 states have implemented some form of education tax credit scholarship program. The programs vary dramatically in generosity, accessibility, and structure. Let me highlight the major players:

Arizona leads the pack with its Empowerment Scholarship Account program, which allows families to receive a portion of per-pupil funding to spend on education expenses (private school tuition, tutoring, special services, even homeschool curriculum). The account is funded through a tax credit scholarship—donors get a credit against Arizona income taxes.

Florida‘s Step Up For Students program is similarly generous, offering both the Florida Tax Credit Scholarship (funded through corporate tax credits) and the Education Savings Account. These programs serve hundreds of thousands of students.

Indiana, Iowa, Louisiana, Oklahoma, and Pennsylvania all have active tax credit scholarship programs with varying income limits and funding levels. Some prioritize low-income families; others are more open-ended.

The key point: if you live in a state with a voucher program, you may have access to education funding that’s completely separate from federal credits. This is where strategic planning with a corporate tax planning professional becomes essential—especially for business owners who can coordinate personal and business tax strategies.

Claiming Education Credits

Claiming federal education credits requires Form 8863 (Education Credits), which you attach to your Form 1040. The process seems straightforward—list the student’s information, enter qualified education expenses, and calculate the credit. But the devil is in the details.

First, you must have a Form 1098-T from your educational institution. This form reports the qualified education expenses paid during the tax year. However, the Form 1098-T doesn’t always capture all eligible expenses, and sometimes it includes non-qualifying expenses. You need to verify the information independently.

Second, you must determine which credit provides the greatest benefit. The AOTC is typically superior because of its $500 refundable portion, but it phases out at higher income levels. The Lifetime Learning Credit has higher phase-out thresholds but provides less total benefit. Running both scenarios is standard practice.

Third, you cannot claim education credits for expenses paid with scholarship money (unless the scholarship was taxable income to the student). This is a common error—families receive a scholarship, pay tuition, and try to claim a credit on the full amount. The IRS will deny that claim.

For state programs, the claiming process varies. Some states have a separate form or process; others integrate it into the main state income tax return. You’ll need to coordinate with the scholarship-granting organization and understand your state’s specific requirements.

Common Mistakes to Avoid

After years of tax practice, I’ve seen the same education credit mistakes repeated constantly. Let me save you from these pitfalls:

Mistake #1: Double-dipping on expenses. You cannot claim the same expense under multiple credits or claim an expense that was paid with scholarship money. If your child received a $10,000 scholarship and you paid $12,000 in tuition, you can only claim a credit on the $2,000 out-of-pocket expense.

Mistake #2: Ignoring income phase-outs. The AOTC begins phasing out at $80,000 (single) or $160,000 (married filing jointly). If your income is $95,000, you don’t get the full credit—it’s reduced. Many families discover this when filing and lose thousands in expected credits.

Mistake #3: Confusing eligible expenses. Room and board, student activity fees, and transportation are not qualified education expenses for federal credits (though they may be for state programs). Only tuition, fees, and required course materials count. This is a frequent source of IRS denials.

Mistake #4: Not considering the Lifetime Learning Credit for non-degree students. If your child is taking a vocational course or certification program that’s not leading to a degree, you might be ineligible for AOTC but eligible for Lifetime Learning. Many families miss this entirely.

Mistake #5: Failing to coordinate with dependent claims. If your child is claimed as a dependent, they cannot claim education credits themselves. Only the parent/guardian can claim them. But if your child is self-supporting and not claimed as a dependent, they can claim their own education credits. The dependency status matters.

Smart Planning Strategies

Now that you understand the mechanics, let’s talk strategy. How do you maximize the value of education credits and voucher programs?

Strategy #1: Time your education expenses strategically. If you’re in a lower-income year (perhaps due to a job change or business downturn), that might be the optimal year to incur education expenses and claim credits. Conversely, if you know your income will be lower next year, deferring expenses might be beneficial.

Strategy #2: Coordinate federal and state benefits. If you’re in a state with a voucher program, investigate whether you can use both the state tax credit scholarship and federal credits. Some states allow this; others have restrictions. A tax credit certificate from your state might provide additional planning opportunities that work in conjunction with federal benefits.

Strategy #3: Consider the Coverdell Education Savings Account (ESA). While not a tax credit, the Coverdell ESA allows tax-free growth on education savings. You can contribute up to $2,000 annually per beneficiary under age 30. The earnings grow tax-free if used for qualified education expenses. This can be combined with federal credits for a powerful one-two punch.

Strategy #4: Evaluate 529 plans carefully. State 529 plans offer tax-deferred growth and tax-free withdrawals for qualified education expenses. Some states offer an income tax deduction for contributions, which stacks with federal education credits. This is particularly valuable for families with significant education expenses over multiple years.

Strategy #5: Business owners should explore education benefits. If you’re self-employed or own a business, you might be able to establish an educational assistance plan under Section 127 of the tax code, allowing employees (including yourself) to receive up to $5,250 in tax-free education benefits annually. This is separate from and can complement personal education credits.

Frequently Asked Questions

Can I claim both the American Opportunity Tax Credit and the Lifetime Learning Credit in the same year?

Not for the same student. You must choose one credit per student per year. However, if you have multiple students, you could claim AOTC for one and Lifetime Learning for another. The choice should be made based on which provides the greater benefit given your specific circumstances.

What happens if my income exceeds the phase-out threshold for education credits?

The credit is reduced proportionally as your income rises above the threshold. Once you exceed the upper limit (currently $90,000-$100,000 for single filers, $180,000-$200,000 for married filing jointly), you cannot claim the credit at all. This is where strategic income planning becomes valuable—sometimes deferring income or accelerating deductions can keep you under the threshold.

Are education expenses for graduate school eligible for federal credits?

The American Opportunity Tax Credit is only available for the first four years of post-secondary education. Graduate school expenses would need to be claimed under the Lifetime Learning Credit. However, some state voucher programs do cover graduate education, so you’ll need to check your specific state’s rules.

Can I claim education credits if my child received a full scholarship?

Only on the portion of expenses not covered by the scholarship. If the scholarship covers all qualified expenses, you have no eligible expenses to claim a credit on. However, if the scholarship doesn’t cover room and board (which isn’t a qualified expense for federal credits anyway), that doesn’t create an opportunity for credits.

How do state education tax credit scholarships affect my federal taxes?

This depends on the structure. If you donate to a scholarship-granting organization and receive a state tax credit, the donation may not be deductible federally (since you received a credit, not a true charitable deduction). However, the state tax credit itself reduces your state income taxes, which can affect your federal return if you itemize deductions. This is complex and warrants professional review.

What if I paid education expenses in 2024 but my child doesn’t start school until 2025?

Generally, education credits can only be claimed in the year the expenses are paid. If you paid tuition in 2024 for enrollment in 2025, you claim the credit on your 2024 return. However, some educational institutions allow you to pay tuition in advance without triggering the credit until the year of enrollment. Check with your school about their specific policies.

Are there education credits available for K-12 private school tuition?

Federal education credits (AOTC and Lifetime Learning) only apply to post-secondary education. However, many state voucher programs do cover K-12 private school tuition, and some states allow tax-free withdrawals from 529 plans for K-12 expenses. This is another area where state-specific planning is critical.

Can self-employed individuals claim education credits for professional development?

Federal education credits are generally limited to degree-seeking education. However, the Lifetime Learning Credit can cover certain non-degree courses if they improve or maintain job skills. For self-employed individuals, professional development expenses might be deductible as business expenses rather than eligible for education credits. You should evaluate which approach provides greater tax benefit.

Conclusion

The national school voucher program tax credit landscape is complex, but it’s also incredibly valuable for families willing to understand the rules. You’re looking at potential tax savings ranging from $2,000 to $5,000+ per year, depending on your situation, state of residence, and income level. That’s not pocket change—that’s money that could pay for additional education services, reduce your overall tax burden, or fund other financial goals.

The key takeaway is this: there’s no one-size-fits-all approach. Your optimal strategy depends on your income, family situation, state of residence, the type of education expenses you’re incurring, and your overall tax picture. This is why so many families benefit from working with a qualified tax professional who understands both federal and state education incentives.

If you’re navigating education costs, don’t assume you know what credits or programs you qualify for. The rules change annually, new state programs emerge, and income phase-outs shift. Taking time to understand your specific situation—or having a professional review it—could result in thousands of dollars in tax savings. That’s worth the effort.